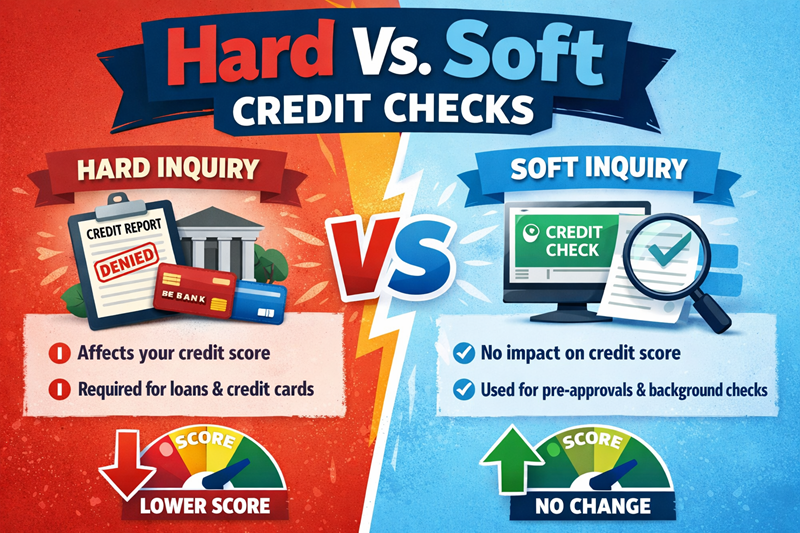

When applying for a loan, you spot two searches. They are known as soft and hard credit checks. Soft credit assessment occurs when a loan company makes an initial enquiry about your credit history. It does not affect your credit score.

Alternatively, hard credit checks are a full examination of your credit report to analyse the actual amount you can afford to repay. It lowers your credit score by 5-10 points for 12-24 months. Unlike soft credit checks, it is visible to everyone who checks your credit score for a loan, credit card or employment purposes.

So, how can you protect your credit score if hard credit checks affect it? Let’s understand.

What is a credit check?

A credit check, also known as a credit search, is when a loan provider looks at your credit report to analyse your financial and payment behaviour. Sometimes, you need to provide your consent to the person undertaking the credit check.

It helps the loan company analyse the amount you can afford to repay. It also helps you understand the right amount. How much can you approximate to borrow without affecting your finances and budget? It is a legal and mandatory process that every financial entity may conduct before the final decision.

Hard Vs. Soft credit checks

Hard credit checks occur during the formal loan applications and are visible to creditors for up to two years. It lowers your credit score by a few points for that term. Thus, taking on hard credit checks multiple times within a short duration is not ideal.

Soft credit checks on the other side are mainly used to compare loan quotes or to get pre-approvals. It helps you understand the basic loan costs without affecting your credit score.

Most loan companies start with a soft credit assessment to check your eligibility for the loan before conducting the hard credit check. Moreover, a hard credit assessment happens only if you decide to proceed with the basic quote you get.

How to protect your credit score during a soft credit check?

As mentioned above, soft credit checks do not affect your credit score in general. It implies you can use the facility multiple times without worry. Still, you can take a few steps to conduct a soft credit check the right way:

● Use a loan eligibility checker

An eligibility checker helps you understand the chances of getting a loan without impacting your credit score. You can use one from MoneySavingExpert, Tesco Bank, Compare the Market or the respective loan company. For example, if you need to pay a credit card bill urgently but you lack enough cash, don’t apply directly.

Instead, check the eligibility first. It could be an ideal approach, especially for individuals with bad credit history. You may get short-term loans from a direct lender for a bad credit score if you meet the eligibility requirements. You can use the eligibility checker for free.

● Ensure updated information

Applying with outdated personal information leads to loan rejection. Thus, always check the name, email, contact number, and residential address before applying. It should be the latest and true to your knowledge. Your rental, employment and payment history must be updated.

● Income should be clear

The inability of the loan provider to analyse your income also affects the chances of getting a loan. Therefore, analyse whether you have a valid income. Do you receive it from a verified bank account? It should be a company’s account and not an individual’s. It is regardless of whether you earn part-time or full-time.

● Use only one bank account for expenses

Most loan providers struggle to calculate your monthly expenses if you use multiple bank accounts for that. Thus, use only one bank account for your basic expenses like rent, groceries, utility bills, mortgage, etc. It helps you generate a decent payment history and improve your credit score. Moreover, it makes it easy for the person to evaluate your affordability.

How to protect your credit score during hard credit assessments?

A hard credit assessment involves a comprehensive review of your finances, debts and income. The loan providers analyse 6 years of repayment history, employment, and residential history. They check financial associations, public records and electoral roll status. Here is how you can protect your credit score during hard credit checks:

● Check and report credit delinquencies

Analyse your credit report before going for a hard credit assessment. Check the pending debts and delinquencies, like paid debts. Report them to the credit agencies and request an updated credit report. It may help you buy some more time before applying.

● Settle your CCJs

A loan company may issue a CCJ if you default on the loan. Having too many County Court Judgements affects the ability to qualify. Thus, check whether you can get a “paid status” on them. For that, you would need to repay the dues according to the dates decided by the court.

If the deadline extends, check how much you owe and clear the CCJs. It may help you get better terms on your next loan. For example, you may get bad credit loans for cars at low interest rates if your credit improves. It reduces the overall payment and monthly instalment costs.

● Address employment gaps

If you have been inconsistent with earnings, it may also impact your credit score during the hard credit assessment. Therefore, address the employment gaps with a letter. Check the format online and write one. It should be concise, focused and with a relevant reason. List the period of unemployment and inconsistent jobs with reasons. It should be true to your knowledge.

● Improve credit utilisation

Try to pay off some debts, improve your monthly income and invest money to improve the credit utilisation ratio. Begin by paying the most expensive debts like credit cards, overdrafts and rent. It immediately brings the ratio down. Try to keep the ratio to 40% and don’t extend it unnecessarily.

Bottom line

Thus, getting a loan requires you to understand hard and soft credit searches in detail. Soft credit search helps you compare loan quotes or pre-qualify without affecting your credit score. It is a mandatory process that you cannot ignore.

Moreover, a hard credit check temporarily dips your credit score and proves helpful in a detailed credit assessment. One must go for a hard credit assessment only if they can afford the initial quote they receive.

Frequently Asked Questions (FAQs)

Do soft checks affect my score?

No. They are only seen by you and have zero impact.

How long do hard searches stay on my report?

Hard searches generally stay for 12 months, though some can remain for up to two years.

Does checking my own credit score hurt it?

No, checking your own report is a soft check.

Can a company check my credit without my permission?

No, a hard check requires your consent, usually through a formal application.

What if I have too many hard checks?

Lenders may view you as high-risk, making it harder to get credit.

Anna Johnson has more than 11 years of experience in direct lending industry of the UK. She is the Senior Content Editor at 24cashflow where she is leading a large team of loan experts. During her career, she has helped the loan aspirants to use the particular loans in the best way and improve their financial lives and status.

Anna Johnson is known for her in-depth research of the UK loan marketplace, as she has worked with many major lending firms in her career. During her educational phase, she has done a research on ‘Finance Fundamentals for Growing Business’.